Your Super Isn't Just a Number.

Most Australians check their super balance the same way they check the petrol gauge: glance at it, hope it's fine, move on.

The problem is that with petrol, running low has immediate consequences. With super, the consequences come thirty years later, when there's not much you can do about it.

This isn't a lecture about saving more. It's a practical explanation of what your super balance actually means, and what the numbers in your statement are telling you if you know how to read them.

The Balance Isn't the Whole Picture

Your account balance is one number. What you'll actually retire on is a different number, and they're rarely the same.

Two things erode the gap between now and retirement:

Fees. Most Australians are paying fund administration fees, investment fees, and often insurance premiums they've never reviewed. Even a difference of 0.5% in annual fees compounds significantly over twenty or thirty years. A $200,000 balance paying 1.5% in fees versus 1% will cost roughly $30,000 over twenty years, assuming average returns. That's before accounting for what that $30,000 would have earned if it had stayed invested.

Investment option. If you've never actively chosen an investment option, you're in your fund's default. Default options vary widely between funds. Some are genuinely well-designed; others are conservative in a way that costs you growth during the years it matters most. Your age, your other assets, and your retirement plans all affect what the right option looks like. It's rarely a one-size-fits-all answer.

The Contribution Picture

Super contributions come from three places:

Your employer (currently 12% of your ordinary time earnings)

Salary sacrifice (additional contributions made pre-tax from your wage)

After-tax contributions (money added from your bank account)

The concessional (pre-tax) contributions cap is $30,000 per year (increasing to $32,500 from July 2026). That includes employer contributions. So if your employer puts in $15,000, you can currently add up to another $15,000 in a tax effective way.

Many people are unaware of the unused cap carry-forward rule: if your super balance is under $500,000, you can carry forward unused concessional contribution space from the previous five financial years. This is particularly useful after a career break, or if you've recently started earning more and want to be tax effective.

Insurance Inside Super

Most super funds include default life insurance and total and permanent disability (TPD) cover. For select people, this is useful, affordable cover. For others, it's a drain on their balance for a product that doesn't fit their situation, or that overlaps with cover they're already paying for elsewhere.

It's worth checking:

What cover you actually have

What the premium costs per year

Whether the definitions in the policy (particularly TPD definitions) match what you'd actually need

Whether you're insured under multiple funds paying premiums twice

You can opt out of insurance inside super if it doesn't serve you. You can also review whether the cover you have is the right type and amount.

What "On Track" Actually Means

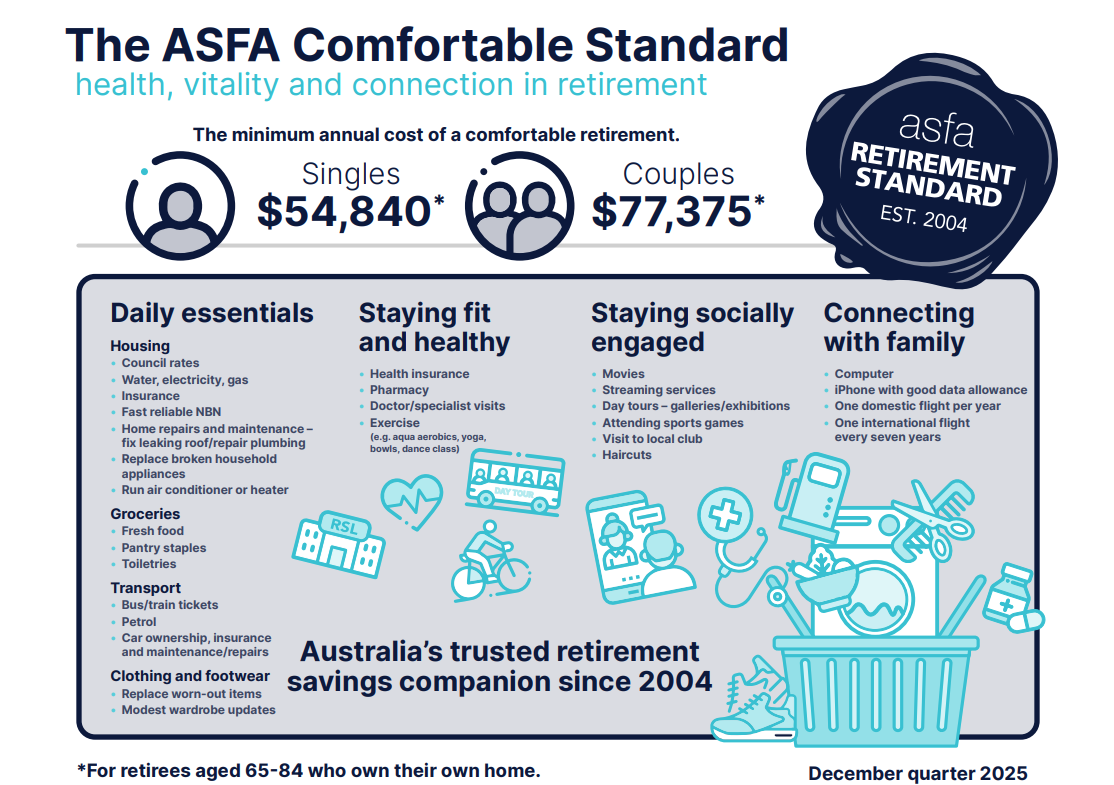

There's no single answer to what you need at retirement. It depends on what kind of retirement you're planning for. But the Association of Superannuation Funds of Australia (ASFA) publishes a useful benchmark: as of their most recent figures, a comfortable retirement for a couple requires roughly $730,000 in super at age 67, assuming they own their home outright. For a single person, around $630,000.

A modest retirement covering basic needs requires significantly less. But most people, when asked, want something closer to comfortable.

The way to check whether you're tracking toward your number is to use your fund's online calculator or speak with a financial adviser. What you're looking for is a projection based on your current balance, your contribution rate, your investment option, and your expected retirement age. A meaningful projection also accounts for inflation.

The Practical Starting Point

For anyone who has never actively engaged with their super, here are the four things worth doing first:

Consolidate any old super accounts you're not using. Every account with a balance is paying fees and potentially premiums. Although, you need to be keenly aware of any potential benefits you may unintentionally lose when closing or consolidating accounts.

Check your investment option and understand what it's invested in.

Review your insurance cover and confirm what you have, what it costs, and whether it fits your situation.

Check your beneficiary nomination. Super doesn't automatically form part of your estate. An outdated or lapsed nomination can have serious consequences for the people you leave behind.

This article is general information only and does not take into account your personal circumstances. Before making any changes to your superannuation, speak with a licensed financial adviser.